Albert Einstein said, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” The whole idea of investing is to take advantage of compound interest. A few general principles to live by are:

- Pay off all debt so you don’t have compounding interest working against you.

- Keep costs low.

- Be tax efficient.

- Passive over active management (passive management is less expensive and usually has higher returns than active management)

- Don’t try to beat the market, be happy with getting the returns the market provides. Be ok with tracking the market.

- Employee match: you must take full advantage of any employee match plan. It is free money, do it! Even if the funds that are offered aren’t that good or charge a higher expense ratio it is still worth it to get the full company match whenever it is offered.

- Invest in Index funds. Index funds are (1) low cost, (2) low turnover, (3) tax efficient, (4) passively managed and (5) they track the market well. If you invest in index funds you will beat 2/3 of all mutual funds in the same market in any given year and the odds of an index fund beating any actively managed mutual fund go up the longer one stays in the index fund. This is mostly because the expense ratio of index funds is so much lower than actively managed.

Debt

Pay off all debt so you don’t have compounding interest working against you. Easier said than done. You must prioritize, and credit card debt is usually the worst of all types of debt. For young physicians student loans are right up there. Many resident physicians have six figure student loan debt. There are a lot of books dedicated to getting out of debt and the debate of “good” versus “bad” debt. All debt is bad, all debt should be paid off, but when to pay off debt vs. defer debt payments to try to invest some money is unique to each individual. Some prefer to pay off all debt before they start to invest. Others prefer to start to invest earlier. If nothing else, those who invest earlier are at least learning how to do it, learning to pay themselves first and live off less income and setting up a routine of investing that will work well when they become an attending physician with a significantly higher income.

Even if you can’t invest now you should be ready to invest once you make more money as an attending. It might be worth starting a small investment portfolio now so that you can learn how to do it before you have more money at risk.

Buyer Beware

Beware of management fees. Any money you pay an advisor is money that leaves your account and goes into his or hers. Most advisors will charge a percentage of assets under management (AUM). No matter how your funds perform they will get a percentage of all your assets. This is very good for them, not so good for you the investor.

Beware of expense ratios. Each mutual fund or index fund will charge an expense ratio. Running a mutual fund with advisors trying to buy low and sell high costs money and these are smart people that get paid well. There are lots of people involved and they all get a paycheck and you the investor pay them for this “service”. Some of that money is collected from you the investor as an expense ratio. Expense ratios are often in the 1-2% range. That means that for every $100 invested 1-2%, is taken out every year, regardless of performance. Index funds expense ratios are often 0.10% and can be as low as 0.05%. Obvious advantage here for the index funds.

Beware of turnover. Turnover refers to how often the assets in a fund are bought and sold each year. If a fund has $100 million dollars of assets and trades $100 million dollars worth in a given year the turnover for that year is 100%. Why do you care about turnover? Because higher turnover means higher taxes. If your mutual fund manager buys low and sells high for a profit that profit can be taxed as either income or capital gains, and the IRS will tax those gains. You can protect yourself from taxes by putting these high turnover funds or tax-inefficient assets into your tax-protected accounts, or by buying low turnover funds, such as index funds. Advantage index funds.

Diversification

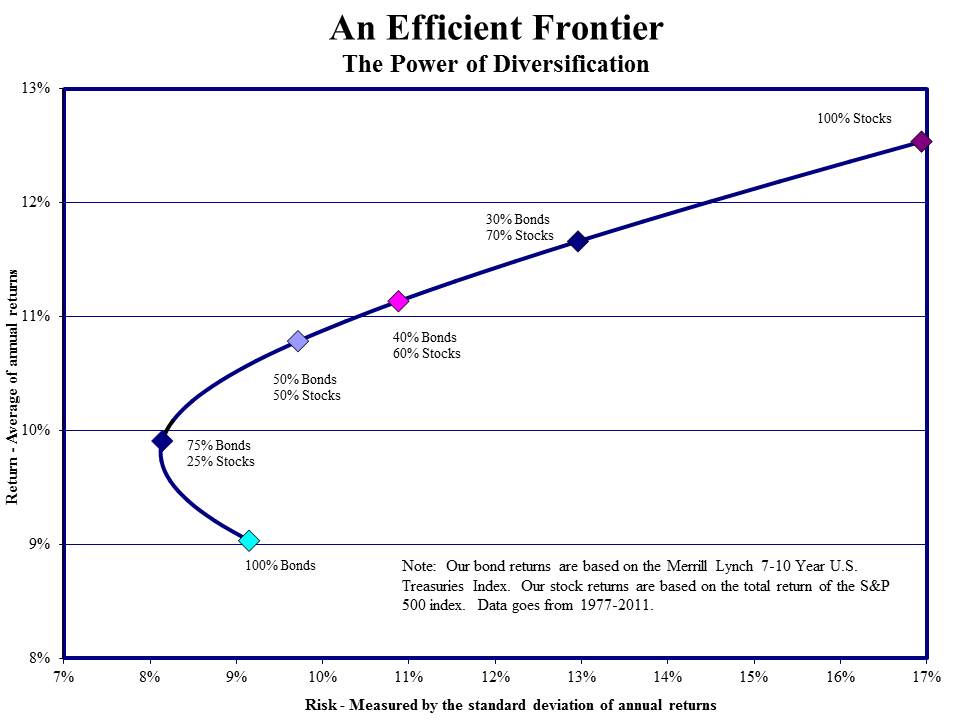

If you find yourself thinking that only investing in stocks is a good idea because they have the highest projected returns, I want you to think about risk versus return. Adding some diversification, i.e. with bonds, can significantly lower your risk without significantly lowering your return. There is a concept called the efficient frontier. The general concept can be thought of in this way. We all want the highest possible return with the lowest possible risk, but these “free rides” don’t exist in the real world. We want to be as close to the top left of the risk vs. reward graph, seen below, as possible. The efficient frontier is based on the idea that the market is efficient. Most investments with higher return also have higher risk. The kicker is that diversification can significantly lower your risk without significantly lowering your return, almost like a free lunch.

The ideal way to diversify a portfolio is to buy assets that are negatively correlated, i.e. when one asset increases in value the other decreases in value. Although stocks and bonds are not truly negatively correlated, they are relatively poorly correlated. If one diversifies to invest in both stocks and bonds, if either one does poorly the other usually does well protecting your overall portfolio. Index funds are inherently diverse as they buy stocks from every company in the market. So a total US stock market index fund actually buys stocks from all publicly traded U.S. companies—approximately 5,000 companies—weighted based on their market share. The S&P 500 index fund buys stocks from all 500 companies listed in the Standard and Poors top 500 list, i.e. the S&P 500, again, weighted based on their market share. To really diversify a portfolio one should have at least three types of assets: U.S. stocks, international stocks and U.S. bonds. Diversification is important because diversification mitigates risk.

Asset Allocation

So where should I put my assets? Should I have some bonds, some international stocks, what percentages do I need in each asset class?

Like so many other investment decision this is based on your risk tolerance. There is an old rule that states one should have their “age in bonds.” So a 30-year-old resident should have 30% in bonds. This is an older rule and with people living longer these days this might be too conservative. Also, being that we are all in healthcare and physicians often have better job stability, a more aggressive and stock heavy investment plan might be better. Most money for a younger investor should be in the U.S. stock market, followed by international stocks and then by U.S. bonds. An asset allocation for a 30-year-old resident physician might look like: 70% U.S. Stocks, 20% international stocks, 10% U.S. bonds.

Target Date Funds

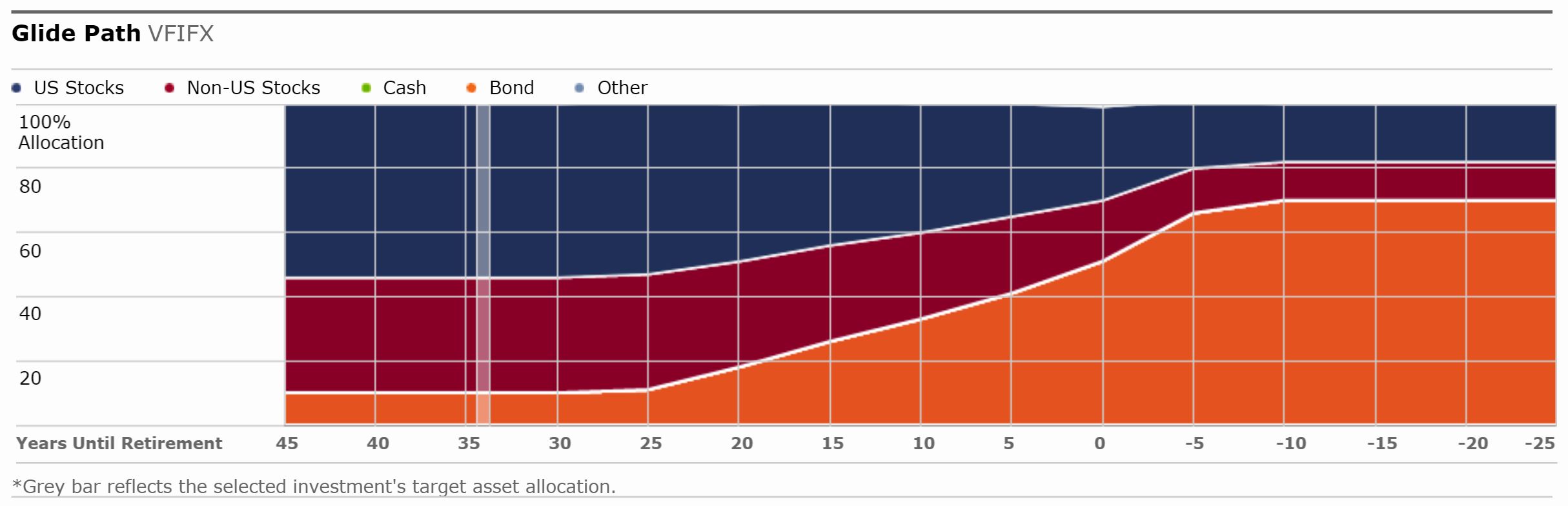

You can also refer to “target date” retirement funds and see the asset allocations they have. Target date funds do all the asset allocation work for you. They still invest in index funds, which is good, but they do the rebalancing for you. They rebalance by getting more conservative as one gets older and closer to retirement. In retirement we will start to live off the investments and no longer have a job that enables us to grow our investments. In retirement a stock market crash would be harder to recover from than it would for someone with 20 working years left. So we rebalance our portfolio as we age. In retirement we are protected from a stock market crash by having a larger percentage of our assets in bonds. The Vanguard target date fund 2050, ticker VFIFX, for someone that is 30 years old in 2016 is set for a planned retirement in 2050. The percentages breakdown for the Vanguard target date fund 2050 at inception is approximately 55% U.S. stock, 35% international stock, 10% U.S. bonds. Near retirement this changes to approximately 30% U.S. stock, 20% international stock, 50% U.S. bonds. Below is an graph that shows the asset allocation from a target date fund and how it changes with time.

The diagram above is for a target date fund for someone who plans to retire in 2050. For a 30-year-old resident in 2016 that would mean retiring at age 64. What you will notice from the diagram above, is that the funds starts out with more stocks early on and becomes more conservative with time adding more bonds as one gets closer to their retirement age. Target dates funds like the one above are rebalanced by the fund manager to become more conservative with time.

The Simple 3 Fund Portfolio Concept

At this point we know we need to keep costs low, not try to beat the market, keep transaction volume low and have some type of plan for rebalancing our portfolio to adjust to our changing risk tolerance. A target date fund, like the one referenced above, will do all of this for you. Granted since you are having a fund manager rebalance your fund, you will have slightly higher expenses, but these are still really low. Another option is to invest in three separate index funds. This happens to be what I do. The “three fund portfolio” consists of a total U.S. stock market index fund, a total international stock market index fund and a total U.S. bond index fund. You can start off as aggressive as you like and rebalance as you age. Just how aggressive, i.e. how much stock to have, is up to you. Being a physician is stressful enough, so investing shouldn’t be. I recommend you invest to your sleeping point, the point where you sleep well each night and don’t worry about how risky your portfolio is. Regardless of your risk tolerance you will probably rebalance your portfolio as you age. If your U.S. stock index fund does really well one year, you can sell some U.S. stock index fund (sell high) and buy more bonds or more international stock index funds (buy low).

Or you can avoid selling anything and, therefore, avoid realizing capital gains and paying fees associated with selling and just buy more of the asset class that underperformed. In the example above if U.S. stocks did really well compared to international stock index funds and U.S. bond index funds, then your next several purchases can all go toward international stock index funds and U.S. bond index funds. Here you are buying low, rebalancing your portfolio without accruing any capital gains or unnecessary fees and keeping your desired asset allocation to match your risk tolerance. I prefer to re-balance by contributing more to the asset class that is underperforming.

Where Should I Put Each Type of Asset?

Tax inefficient funds should be placed in tax efficient accounts, like your workplace 401k or 403b where they can grow tax deferred. Tax efficient assets can then be placed in your taxable accounts, like your private Vanguard or other brokerage account. If you don’t max out your 401k/403b or IRA contributions and don’t think you will need the money before retirement age, then you can of course place tax efficient assets in tax-deferred accounts. If you are thinking of retiring early, make sure to have some money in non-retirement accounts so you can withdraw the money without penalties. The most tax efficient of the 3 assets we have been talking about are U.S. stocks, followed by international stocks with bonds being the most tax inefficient.

If you want to do a simple three fund portfolio you can place your bonds in your 401k/403 tax-deferred account, then place your international stocks in the 401k/403b account if you have any more room before you reach your max contribution, then place your U.S. stocks in your taxable accounts.

The 3 Fund Portfolio Asset Allocation

- Total U.S. Bond Market Index Fund ➔ 403b

- Total International Stock Market Index Fund ➔ 403b until full then into Roth IRA then into taxable account

- Total U.S. Stock Market Index Fund ➔ Taxable account

Where Can I Get More Information Like This?

There is plenty of information out there, but reader/buyer beware. Beware of who is writing it, beware of what they are selling. I have listed a few books below that I have found to be the most helpful and the easiest to read.

- The Little Book of Common Sense Investing by John Bogle. John Bogle created the first index fund. He also founded Vanguard, which is the only mutual fund company owned by its investors, not shareholders, and is known for low costs. The “Bogle” way is all about keeping fees low, passive is better than active management, and don’t try to beat the market, just track it.

- The White Coat Investor by James M. Dahle, MD. This is a good book written by one of our own. It is aimed at younger physicians and like Bogle’s book promotes low-cost funds.

- The Bogleheads’ Guide to Investing by Mel Lindauer, Michael LeBoeuf, and Taylor Larimore. As the name implies this book supports the “Bogle” way of investing.

Resident Physician Contributing Writer

Beaumont Health System

Born and raised in a small town, Dr. Nasmyth Loy earned his first dollars by doing chores around the house as a child. After overhearing his grandmother talking about money and learning more about the art of financial investing from his parents, he was hooked. He started investing every dollar he could and -- more than twenty-five years later -- he still makes investing a priority. Following college, he worked in financial consulting and real estate before deciding to enter medical school. He is now an orthopaedic surgery resident and lives with his wife, a nurse practitioner, and their daughter.